Right now, Chief Compliance Officers at community banks across the country are juggling impossible priorities. They’re managing dozens of competing demands with teams already stretched thin, while trying to interpret the latest CFPB guidance that seems to contradict what was said six months ago. CEOs are asking for cost savings. Boards want ironclad compliance. And somewhere between vendor management, staff training, and exam prep, these professionals must decode what regulators really want.

“Sometimes it feels like I’m flying blind — trying to keep up with regulators while making sure our fintech partners aren’t dropping the ball. We don’t have time to validate everything manually anymore.” — Chief Compliance Officer, $2B Community Bank

The mixed signals from Washington create a unique challenge for community banks. Every CCO is wrestling with the same fundamental question: How do you build a compliance program that’s both effective and efficient when regulatory priorities keep shifting?

Here’s what successful community bank compliance programs have discovered:

The goal isn’t to predict the future. It’s to build a framework for making smart decisions regardless of what the future brings.

This guide provides three practical decision frameworks designed specifically for community banks—where every dollar counts and every hour matters.

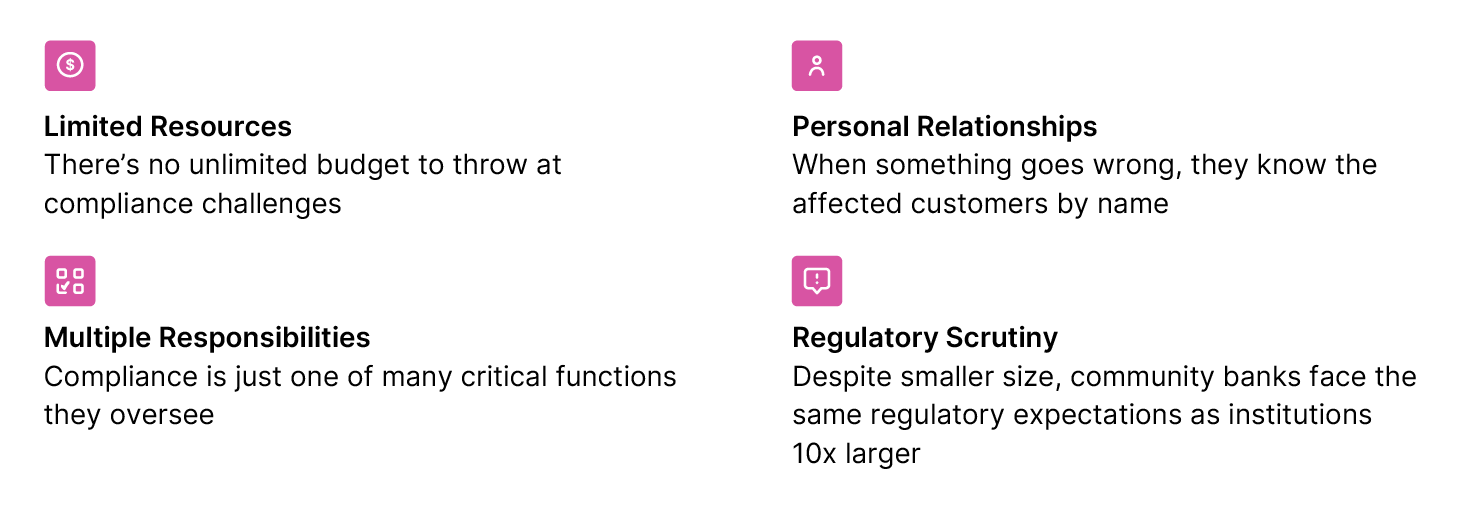

Community bank CCOs face unique challenges that larger institutions don’t always understand:

The natural response to regulatory uncertainty? Analysis paralysis.

But while some wait for clarity, competitors move forward and risk exposure grows.

The truth is: In community banking, uncertainty isn’t the enemy—indecision is.

With a small team and tight budget, where should compliance resources be focused for maximum impact?

You can’t cover everything equally. The smartest CCOs focus where the stakes are highest — and find creative, efficient ways to cover the rest.

Step 1: Assess the Bank’s Unique Risk Profile

Ask yourself the following questions about your risk profile:

• Which products generate the most revenue but carry compliance risk?

• Where have peer banks of similar size seen enforcement actions?

• What risks would cause the most damage if they materialized — financially or reputationally?

Step 2: Evaluate Current Control Reality

Ask yourself the following questions about your current controls:

• Where do manual processes consume excessive time?

• Which controls depend on one key person (single point of failure)?

• What breaks when someone is on vacation?

Step 3: Decide Where to Spend Your Time

Plot each risk area, along with the current control evaluation, on this chart to decide where to spend your time, or use our decision tree to help you.

The Community Bank Insight: Excellence in everything isn't possible. Focus relentlessly on what could hurt the bank or customers most.

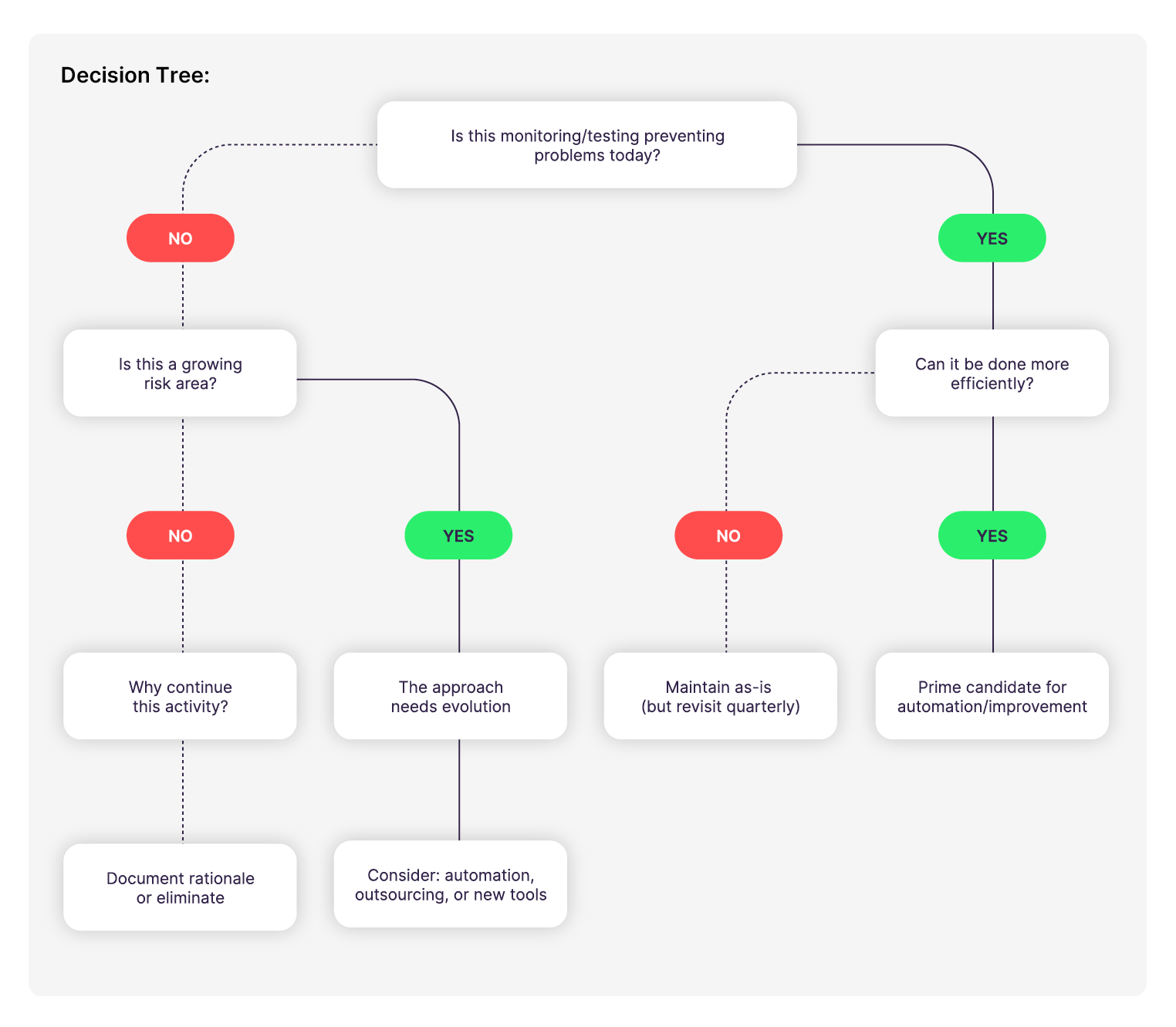

How should monitoring and testing evolve to stay ahead of risks without breaking the budget?

At many community banks, monitoring and testing hasn’t changed much in a decade. But the risk landscape has. Complaints come in faster. Digital products create new exposure. Regulators expect more proof of proactive oversight. So how do you scale without just throwing more people at the problem?

Step 1: The Non-Negotiable Foundation

For your particular business type and product offering, consider the following things:

• Are there legal minimum requirements for our charter type?

• Which areas have had past findings or violations?

• Do we have products touching vulnerable populations?

• Are there any customer complaint patterns?

Step 2: Growth Opportunities

Consider where your current processes could benefit from improvement by asking the following things:

• Could we do this in a more proactive way?

• Can we automate this process?

• Do we need to, and can we, create consistency across products?

• How do we build institutional knowledge that stays with the bank?

Step 3: Decide Where to Spend Time

Use our decision tree to allocate your time effectively:

The Community Bank Insight: The goal isn’t to do less—it’s to do more with existing resources. Smart automation and the right tools multiply team effectiveness.

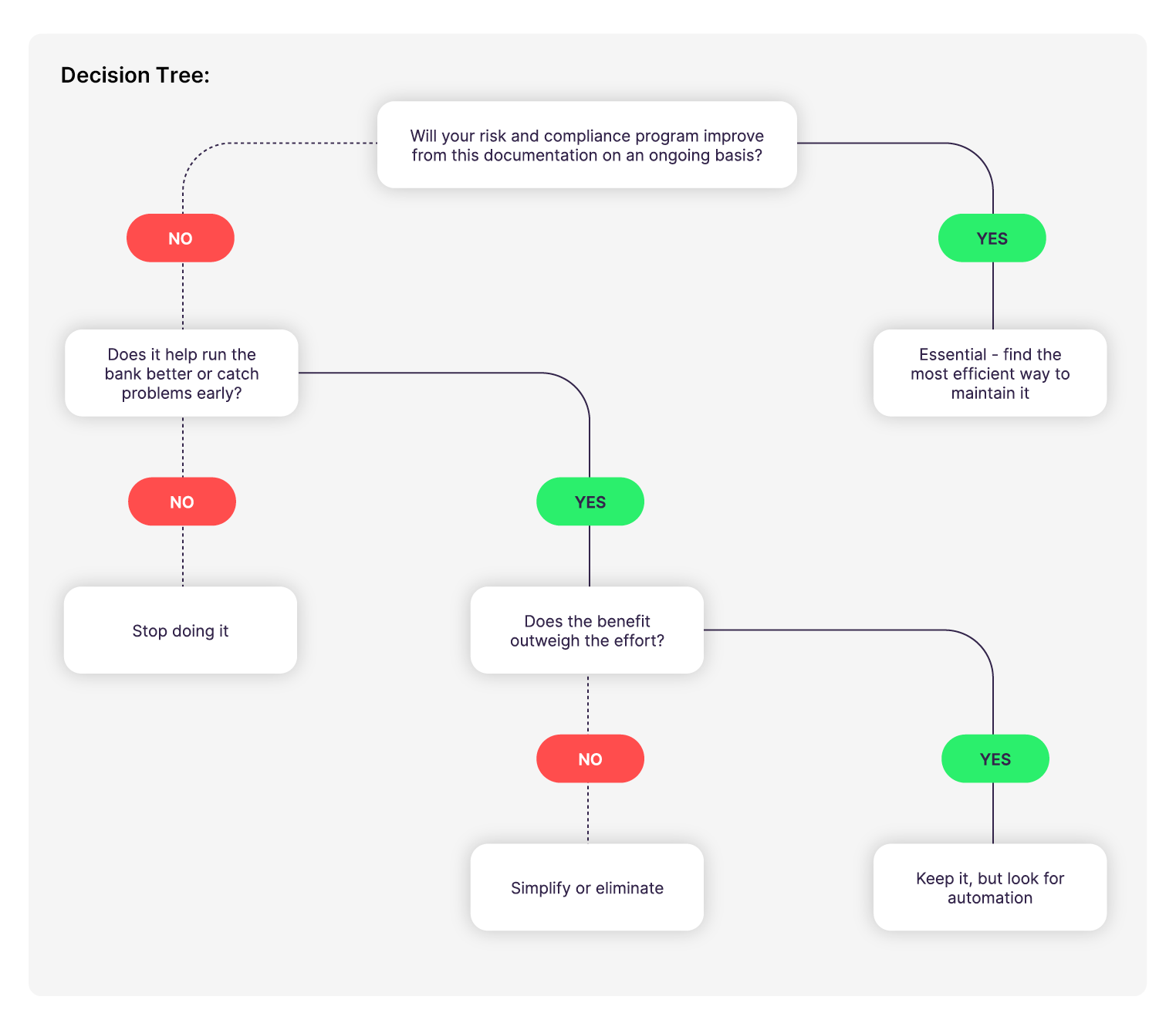

How can documentation serve as both examiner evidence AND a tool for catching problems early?

Documentation is often where CCOs burn out. Boards want thick binders. Staff churn creates gaps. Regulators want to see proof, but not everything is equally valuable. You need to decide how to prioritize producing documentation so you know what can drop if other emergencies come up. Use this hierarchy and decision tree to prioritize your time.

Tier 1: Compliance Essentials

• Required regulatory reports

• Board and committee minutes

• Customer complaint logs with resolutions

• Gap analysis and evidence of corrective actions taken

Tier 2: Risk and Control Documentation

• Process controls and exception tracking

• Training records showing competency

• Vendor oversight documentation and monitoring

• Ongoing risk assessment updates

Tier 3: Proactive Risk Intelligence

• Trend analysis that reveals emerging risks

• Predictive risk indicators and early warning signals

• Benchmarking for performance gaps

The Community Bank Insight: Good documentation tells the bank’s compliance story. Focus on quality narratives over quantity of paper.

Now that you understand the three critical decision frameworks, here’s how to put them into practice:

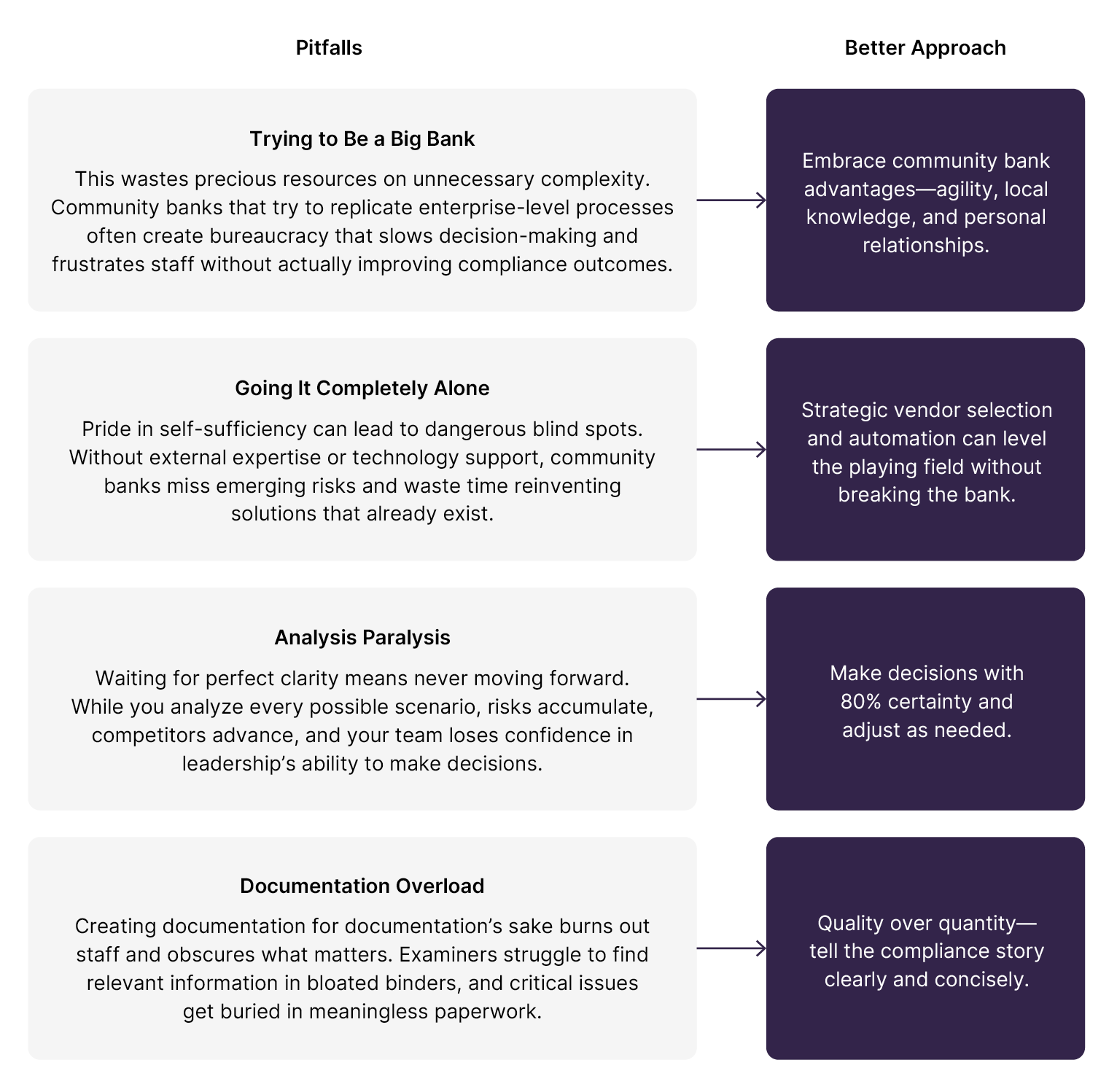

Before implementing these frameworks, watch out for these common traps that derail community bank compliance programs:

Use these questions in your next board meeting or one-on-one with the CEO to start strategic compliance conversations:

1. What’s the institution’s appetite for regulatory risk vs. capacity to manage it?

(Helps establish realistic expectations)

2. Where could strategic technology investment multiply team effectiveness?

(Opens door to automation discussions)

3. How should the bank differentiate itself—as the safest or the most efficient?

(Guides program development priorities)

4. What would a compliance failure cost—in dollars and reputation?

(Creates urgency without fear-mongering)

Pick 1-2 questions most relevant to your current situation.

Don’t overwhelm leadership with all four at once.

Building an effective compliance program doesn’t require unlimited resources. It requires smart frameworks, strategic decisions, and the right tools to multiply impact.

The community bank CCOs who thrive in uncertain times aren’t those with the biggest budgets or largest teams. They’re the ones who make strategic decisions, leverage technology wisely, and focus relentlessly on what matters most for their bank and community.

Success is achievable. And no one has to do it alone. The impact of implementing these frameworks with the right technology support can be transformative.

Cable’s automated control testing and continuous risk assessment platform is built specifically for community banks. The technology multiplies team effectiveness, creates a consistent process across all products, and adapts automatically to regulatory changes—delivering enterprise-level compliance capabilities at community bank prices. When hiring more people isn’t an option, Cable helps existing teams accomplish more.

Breaching the $10B Asset Threshold - Supervision and Examinations

Breaching the $10B Asset Threshold - Supervision and Examinations Breaching the $10B Asset Threshold - Operational Requirements

Breaching the $10B Asset Threshold - Operational Requirements Breaching the $10B Asset Threshold - Governance and Risk Management Compliance Requirements

Breaching the $10B Asset Threshold - Governance and Risk Management Compliance RequirementsRight now, Chief Compliance Officers at community banks across the country are juggling impossible priorities. They’re managing dozens of competing demands with teams already stretched thin, while trying to interpret the latest CFPB guidance that seems to contradict what was said six months ago. CEOs are asking for cost savings. Boards want ironclad compliance. And somewhere between vendor management, staff training, and exam prep, these professionals must decode what regulators really want.

“Sometimes it feels like I’m flying blind — trying to keep up with regulators while making sure our fintech partners aren’t dropping the ball. We don’t have time to validate everything manually anymore.” — Chief Compliance Officer, $2B Community Bank

The mixed signals from Washington create a unique challenge for community banks. Every CCO is wrestling with the same fundamental question: How do you build a compliance program that’s both effective and efficient when regulatory priorities keep shifting?

Here’s what successful community bank compliance programs have discovered:

The goal isn’t to predict the future. It’s to build a framework for making smart decisions regardless of what the future brings.

This guide provides three practical decision frameworks designed specifically for community banks—where every dollar counts and every hour matters.

Community bank CCOs face unique challenges that larger institutions don’t always understand:

The natural response to regulatory uncertainty? Analysis paralysis.

But while some wait for clarity, competitors move forward and risk exposure grows.

The truth is: In community banking, uncertainty isn’t the enemy—indecision is.

With a small team and tight budget, where should compliance resources be focused for maximum impact?

You can’t cover everything equally. The smartest CCOs focus where the stakes are highest — and find creative, efficient ways to cover the rest.

Step 1: Assess the Bank’s Unique Risk Profile

Ask yourself the following questions about your risk profile:

• Which products generate the most revenue but carry compliance risk?

• Where have peer banks of similar size seen enforcement actions?

• What risks would cause the most damage if they materialized — financially or reputationally?

Step 2: Evaluate Current Control Reality

Ask yourself the following questions about your current controls:

• Where do manual processes consume excessive time?

• Which controls depend on one key person (single point of failure)?

• What breaks when someone is on vacation?

Step 3: Decide Where to Spend Your Time

Plot each risk area, along with the current control evaluation, on this chart to decide where to spend your time, or use our decision tree to help you.

The Community Bank Insight: Excellence in everything isn't possible. Focus relentlessly on what could hurt the bank or customers most.

How should monitoring and testing evolve to stay ahead of risks without breaking the budget?

At many community banks, monitoring and testing hasn’t changed much in a decade. But the risk landscape has. Complaints come in faster. Digital products create new exposure. Regulators expect more proof of proactive oversight. So how do you scale without just throwing more people at the problem?

Step 1: The Non-Negotiable Foundation

For your particular business type and product offering, consider the following things:

• Are there legal minimum requirements for our charter type?

• Which areas have had past findings or violations?

• Do we have products touching vulnerable populations?

• Are there any customer complaint patterns?

Step 2: Growth Opportunities

Consider where your current processes could benefit from improvement by asking the following things:

• Could we do this in a more proactive way?

• Can we automate this process?

• Do we need to, and can we, create consistency across products?

• How do we build institutional knowledge that stays with the bank?

Step 3: Decide Where to Spend Time

Use our decision tree to allocate your time effectively:

The Community Bank Insight: The goal isn’t to do less—it’s to do more with existing resources. Smart automation and the right tools multiply team effectiveness.

How can documentation serve as both examiner evidence AND a tool for catching problems early?

Documentation is often where CCOs burn out. Boards want thick binders. Staff churn creates gaps. Regulators want to see proof, but not everything is equally valuable. You need to decide how to prioritize producing documentation so you know what can drop if other emergencies come up. Use this hierarchy and decision tree to prioritize your time.

Tier 1: Compliance Essentials

• Required regulatory reports

• Board and committee minutes

• Customer complaint logs with resolutions

• Gap analysis and evidence of corrective actions taken

Tier 2: Risk and Control Documentation

• Process controls and exception tracking

• Training records showing competency

• Vendor oversight documentation and monitoring

• Ongoing risk assessment updates

Tier 3: Proactive Risk Intelligence

• Trend analysis that reveals emerging risks

• Predictive risk indicators and early warning signals

• Benchmarking for performance gaps

The Community Bank Insight: Good documentation tells the bank’s compliance story. Focus on quality narratives over quantity of paper.

Now that you understand the three critical decision frameworks, here’s how to put them into practice:

Before implementing these frameworks, watch out for these common traps that derail community bank compliance programs:

Use these questions in your next board meeting or one-on-one with the CEO to start strategic compliance conversations:

1. What’s the institution’s appetite for regulatory risk vs. capacity to manage it?

(Helps establish realistic expectations)

2. Where could strategic technology investment multiply team effectiveness?

(Opens door to automation discussions)

3. How should the bank differentiate itself—as the safest or the most efficient?

(Guides program development priorities)

4. What would a compliance failure cost—in dollars and reputation?

(Creates urgency without fear-mongering)

Pick 1-2 questions most relevant to your current situation.

Don’t overwhelm leadership with all four at once.

Building an effective compliance program doesn’t require unlimited resources. It requires smart frameworks, strategic decisions, and the right tools to multiply impact.

The community bank CCOs who thrive in uncertain times aren’t those with the biggest budgets or largest teams. They’re the ones who make strategic decisions, leverage technology wisely, and focus relentlessly on what matters most for their bank and community.

Success is achievable. And no one has to do it alone. The impact of implementing these frameworks with the right technology support can be transformative.

Cable’s automated control testing and continuous risk assessment platform is built specifically for community banks. The technology multiplies team effectiveness, creates a consistent process across all products, and adapts automatically to regulatory changes—delivering enterprise-level compliance capabilities at community bank prices. When hiring more people isn’t an option, Cable helps existing teams accomplish more.